Estimated tin production by Myanmar has seen a more than 10-fold increase in the four years to 2015. This is almost entirely due to the rapid growth in a major new mining centre in Wa county, close to the border with China’s Yunnan province.

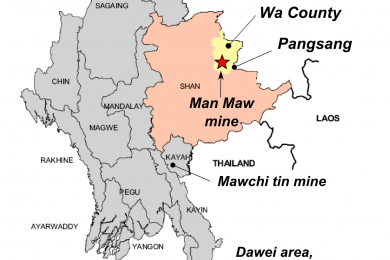

The main mining zone, called Man Maw, covers a 200 km2 area, 90 km north-west by road from the capital Pangsang on the China-Myanmar border. Within this, current mining activity is focussed in a 20 km2 area and these operations now account for some 95% of estimated total national production.

Based on a recent visit to the area by ITRI China staff, it appears that Myanmar tin production is peaking at some 50,000 t/y, although there is still significant potential for the discovery of new ore resources.

Wa county production can be measured by China’s official tin ore and concentrate import data. However ITRI believes that the big increase in imports reported by China in the first half of 2016 (up 88% year-on-year in gross weight terms) is based on a depletion of above ground stocks of ore and concentrate accumulated over the last few years. This masks an underlying decline in mining activity and depletion of readily accessible higher grade ore resources.

Some of the major changes over the last two years observed by ITRI China staff have been:

- In 2014 most production came from several large open pit mines, but these have been largely depleted and today most mining is underground, with higher operating costs and lower ore grades

- Many small mining companies have failed or left the area and the companies who are still involved are generally bigger, better organized and well financed. They have invested heavily in the mechanisation of mining, expanded ore processing facilities and transport and other infrastructure

- While grades of more than 10% were common two years ago, most ore mined now grades between 2 – 3% Sn. A big newly discovered high-grade (7 – 8% Sn) resource was exploited through the second half of last year and the early part of this year, but this is now largely depleted

- Until recently ore grading less than 3% Sn was stockpiled as mine owners sought to make a quick return from the higher grade material. However improvements in processing capacity and technology, and a rising tin price, have now made it economic to treat this stockpile.

In the short-term, output from Wa seems stable but production and shipments will be reduced in the rainy season which began in June and usually continues to October. The longer-term outlook for production in Wa mainly depends on whether there are new resource discoveries in the next few years. Otherwise, production may peak in 2015-2017 and then decline.