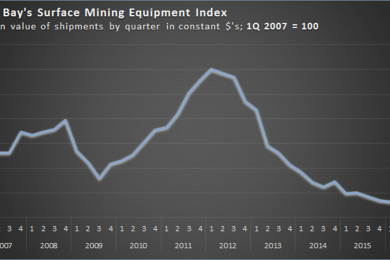

Having reached what appears to have been ‘rock bottom’ of the severe, four-year contraction in large equipment deliveries early in 2016, shipments of large mobile surface mining equipment shipped during the last calendar quarter increased by almost one-third (units) with aggregate value increasing by 28% versus Q3. These gains came on top of significant improvements during the July-September quarter. Coupled with a myriad of other markers of mining industry improvement, this may well signal the beginning of a sustainable growth cycle.

These data are the result of direct reporting of individual machines shipped by the leading manufacturers of large mining trucks, electric/rope and hydraulic shovels/excavators, wheel loaders, crawler and wheel dozers, blast-hole drills and motor graders to The Parker Bay Company, and they underlie Parker Bay’s Surface Mining Equipment Index.

The decline in shipments since early 2012 was extreme and, in that context, the gains during the second half of 2016 appear modest. And some manufacturers are not yet projecting significant improvements in their 2017 sales. Nevertheless, these results are the first clear gains for this group of major production equipment following years of almost relentless declines.

The Index, which tracks shipments of only the largest mobile equipment delivered to the largest surface mines worldwide, covers mines and machines that produce a significant (and in some instances a majority) share of the world’s coal, copper, iron, gold and other minerals. And it is believed to be representative of the mining industry’s new equipment purchasing activities as a whole.

But it does not take into account used equipment that mines have removed from service and reapplied either at their own operations or through resale. This secondary market has accounted for a substantial share of miners’ capacity additions during the current industry down-cycle, and some measures of this market also show signs of improvement. A number of major miners are known to have focused on newer used machines, and Parker Bay says it has identified several instances of large numbers of these units being purchased and applied thus substituting for significant new machine purchases. While these resale opportunities continue, as the number and types of machines available decline, mining companies may be forced to ratchet up orders for new equipment during 2017.

“While there are many dimensions along which to parse the data underlying this Index, taking a somewhat longer-term view reveals several shifts in the parameters of equipment shipments during 2016 versus the preceding five-year period. The relative shares of 2016 shipments by product line are generally consistent with those delivered during 2011-2015 with one notable exception: electric/rope shovel shipments continued to decline sharply while hydraulic shovels/excavators assumed greater shares of miners’ investments in loading tools. This may simply reflect the lesser need to replace the larger and longer-lived electric shovels, something that will be reversed as the expansion cycle transitions to more new mine development. But it may also signal a longer-term decline in miners’ preferences for these highly productive yet high capital-cost machines.”

Within each product group, last year’s shipments generally reflect a shift toward somewhat smaller units. Mining trucks in the 90-110 t payload range accounted for two-fifths of all capacity delivered during 2011-2015 but 53% of aggregate payload delivered during 2016. Above 150 t, the Ultra-class units (290 t plus) retained their historical 25% share of capacity. But the trucks in the 154 to 255 t range, units that accounted for more than one-third of all capacity shipped during the previous five years, declined to just 21% of 2016 shipments. “If this shift among the truck size-classes persists, it may signal an even greater reliance on the Ultra-class units than has evolved over the past decade. One of the underlying reasons for the success of Ultra-class trucks has been a renewed demand for these units by Canadian oil sands mines. These deliveries appear to be the start of what might be a wave of replacement for the first generation of 290 t plus units delivered during 1998-2006.”

Across all product lines, deliveries to Canadian oil sands producers accounted for a substantial 12% of all 2016 equipment deliveries compared to just 2% during 2011-2015. Shipments to coal miners rebounded from the severe declines recorded over the past five years, accounting for more than one-third of the aggregate value of global shipments in 2016. Driving this recovery was a remarkable shift away from traditional major coal producing regions (Australia, Canada, South Africa, USA) to national markets less impacted by environmental issues and driven by both internal and export requirements for their output: India, Indonesia and Russia.

All three countries are major coal producers and collectively they account for about 20% of global coal production. But their equipment requirements accounted for nearly two-thirds of all 2016 deliveries to the global coal sector. While gold miners retained their historical share of shipments during 2016, machine deliveries to copper and iron miners did not yet reflect surging mineral prices for these commodities.

Last year’s shipments experienced regional shifts which appear to reflect the relative importance of replacement demand over the needs to increase capacity. The slow- or no-growth regions of North America and Europe accounted for one fourth of 2016 shipments versus 17% over the previous five years. In contrast, the two largest/fastest growing regions during the Super Cycle — Australasia and Latin America – declined from a combined 47% of 2011-2015 shipments’ value to just 35% in 2016. Russia/CIS miners accounted for a surprisingly higher share of last year’s deliveries – 23% (versus 15% during 2011-15). As with North America and Europe/Mideast, this may simply reflect greater needs in the region to replace older machines including some that date to the Soviet Union era.

“Any improvement in industry shipments is a welcome relief after recent severe contractions, but the more important issue is whether the gains recorded in the second half of 2016 are sustainable and likely to continue in 2017. The surge in mineral prices and the underlying supply/demand balance for coal, copper, gold, iron and other minerals hold the key. Clearly the withdrawal of surplus (generally high-cost) mine capacity, and cancellation or deferral of new production has been instrumental in returning balance to these major commodity markets, and accounted for the sharply higher prices that developed in 2016. Suppliers will undoubtedly respond by bringing some new and incremental capacity online. And these may result in increased orders and shipments. But the more important driver of equipment orders and deliveries in 2017 may well be the need to replace older equipment with new, more productive machines that incorporate a range of performance and cost-saving technologies. For that to happen, miners may only require that markets stabilise at or near current levels.”