The uranium price dropped to 12-year lows in October 2016. Investing News Network (INN), looking ahead, found some companies in the sector have higher hopes for what’s in store in 2017.

INN notes that “without a doubt, 2016 was an ugly year for the uranium industry as its price dropped to 12-year lows of $18.25/lb in October. Since then, the price has made a slight recovery to $18.75/lb – although that’s still almost half of what it was at the end of 2015, at $36/lb. To that end, uranium companies in the sector have unsurprisingly been impacted by the resource’s rock-bottom prices, with some saying things can’t really get much worse from here.

“Of course, the uranium price isn’t the only contributing factor in the industry throughout 2016.”

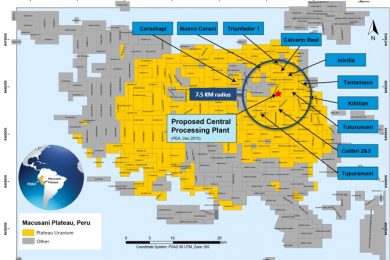

Below, Ted O’Connor, CEO of Plateau Uranium, Craig Parry, CEO of IsoEnergy and George Glasier, Director, President and CEO of Western Uranium shared their thoughts with INN on the 2016 uranium market and gave their uranium outlook 2017. In Peru, Plateau has one of the largest undeveloped uranium projects in the world, shown in the picture.

Asked, at the end of last year (2015), what did you expect from 2016, O’Connor responded: “We had decent hopes for a recovery in uranium market albeit measured.”

Parry: “The resource sector had been in the worst downturn seen in decades at the end of 2015, and we were seeing classic bottom of market events: capitulation of whole sectors; majors selling large assets cheaply; generalists funds leaving the sector; commodity prices at multi-year lows. So we knew we were somewhere near the bottom of the cycle. Being a cyclical business, where low prices are the best cure for low prices, we thought a bounce in the industry wouldn’t be far off.”

Glasier: “We expected the spot price of uranium to be firmer than it is today. We could not anticipate the aggressive selling of byproduct produced material from the majors. We also thought excess uranium inventories would have diminished.”

INN: What had the biggest impact on your commodity in 2016?

O’Connor: “The spot price erosion was primarily due to sellers desperation and underfeeding. Sellers desperate for cash including traders unwinding positions and producers needing to pay their bills with sellers insensitive to price like the US DOE dumping some of their uranium stockpiles to fund legacy clean-up operations. Underfeeding where uranium enrichment suppliers become essentially uranium producers was also an issue because the demand for enrichment services is also less than capacity with most of Japan’s reactors not operating.”

Parry: “The continued weakness in the spot uranium price has been a significant weight on the sector. The spot price is a loud but largely irrelevant data point. However the impact has been that few long term contracts have been written and the spot price is being factored into those negotiations with producers. This has in turn seen significant production cuts both undertaken and planned.”

Glasier: “Supply.”

INN: What was the highlight of 2016 for you?

O’Connor: “For Plateau Uranium, the highlight of 2016 was the completion of our PEA early in the year. The PEA shows we have a project in Peru with lowest quartile uranium production cost potential ($17.38/lb U3O8). We also have lithium resources in the same rocks that will add even more value to the already great uranium story.”

Parry: “There have been a few. We know equities lead the commodity price in any return to bullish market conditions and so the lift in equity prices in November 2016 (Cameco up 40%; NexGen 60%) has been encouraging. I was also very pleased to establish IsoEnergy, which we spun out of NexGen Energy.

“ We raised over $11 million in tough market conditions, built a small but excellent team and have started work on exploring our great portfolio of properties in the eastern Athabasca. Also personally being involved in NexGen as a director the highlights have been numerous. The results the team there has delivered from its Rook I property in the southwest Athabasca Basin are exceptional. The maiden resource from Arrow was the largest ever in the Basin and continued drill results support my view that this is one of the greatest ore bodies ever discovered and will go on to be one of the highest margin mines ever built. And to cap things off the NexGen team has made a couple of more discoveries in the area.”

Glasier: “The highlight of 2016 for the uranium sector was the surprisingly low uranium price. The highlight for Western Uranium was the steady forward movement towards near term production.

INN: What do you expect for the uranium market in 2017?

O’Connor: “For uranium, you can sense the bottom is here. No producers can make money at current spot uranium price and demand will continue to increase due to new reactor builds and more re-starts expected in Japan. Existing and future producers are starting to contract again, at above $40/lb prices, which is well above both the published spot, and term uranium prices.”

Parry: “Leading indicators are pointing to a resurgent bull market. The downturn we have been through has seen little invested in new supply and less in exploration than should have been and this coupled with an improving global outlook for business growth suggests to me that we may be about to enter a bull market that may put the last one in the shade.”

Glasier: “A better market [under a Trump presidency].”

INN: What is your prediction for the uranium price in 2017?

O’Connor: “Uranium prices will improve due to attrition on the supply side with higher cost uranium operations being shuttered and high cost uranium projects being deferred. The uranium price has to increase to incentivize the future production required necessary to meet the increasing demand for uranium.”

Parry: “I think based on the closure of uranium mines and reductions in supply that we will see a strong rebound in spot prices. That said the long-term contracts that are being written now are double the current spot price so we are already seeing the future and where things will head!”

Glasier: “That it will go up 20% [its current price is $18.75/lb].”

INN: What excites you the most about 2017?

O’Connor: “When uranium prices increase, it usually happens extremely quickly and some say ‘violently’. We are living through one of the worst uranium markets ever, and survivors like Plateau Uranium should thrive as the market turns positive. Until then, Plateau continues to sensibly push on in Peru: advancing permitting, drilling, improving our metallurgical understanding and the potential value lithium co-production can bring to the project.”

Parry: “Certainly the end to the 2012-2016 bear market will be worth celebrating. Very much looking forward to getting in and drilling our great targets at IsoEnergy. Also eagerly awaiting NexGen’s second resource announcement.”

Glasier: “For the uranium sector, the 2017 excitement is coming from the US where it is believed the newly elected Trump administration will be much more nuclear power friendly. The market is now acknowledging that with some simple changes to the laws, the US nuclear power industry can undergo a renaissance without compromising safety. Also, Lamar Alexander is leading the Appropriations Subcommittee in Congress to support the nuclear industry. This will have most favourable effects on the USA uranium companies. For Western Uranium in 2017, the company is preparing the assets for production. Many of the mines Western Uranium owns have been past producing mines so the CAPEX to restart production is much lower.”