The ITRI reports that speakers at its 2017 Asia Tin Week in Kunming earlier this month presented different perspectives on the medium-term outlook for China’s tin production, with production expected to remain static or decline slightly in the coming years.

John Johnson, CEO of CRU China, outlined how China’s ‘One Belt One Road (OBOR)’ policy is intended to support the export of commodities in domestic surpluses, such as refined tin, and to import or invest in commodities in deficit such as tin concentrate. Johnson projected that China’s refined tin production in the medium-term would also be supported somewhat by higher prices.

Yue Min, Marketing Director of Yunnan Tin Co, held the view that China’s tin production would be affected by a shortage of tin concentrates as well as higher costs as a result of stricter environmental regulation. Yue believed that secondary tin may play an important role in sustaining production, which would also be driven by consumption growth as a result of China’s urbanization, new applications of tin and the OBOR policy.

Xu Pu, General Manager of Shenzhen Fuyingda Industrial Technology Co, suggested that China’s tin production would be impacted by slower demand growth and higher mining costs as both a result of stricter environmental rules and the deteriorating quality and grade of domestic tin resources.

The ITRI view “is that China’s refined tin production in the medium-term is likely to be directly impacted by declining production and imports from Myanmar. Higher mine production in some areas of China such as Hunan and Inner Mongolia and a partial recovery in secondary tin production is expected but will be unlikely to offset the decline in imported concentrate. We project that China’s mined tin production will decline in the long-term as mining costs rise to due to lower grades and reduced quality of tin resources available for extraction domestically.

ITRI’s 13th annual survey of tin users gathered data from tin users worldwide between June and August 2017. ITRI analyst Tom Mulqueen commented: “latest reports suggest tin usage in chemicals and tinplate in China has been stronger than indicated by our survey results. If this is sustained then it is possible we could see global refined tin consumption growth of around 2% in 2017”

136 companies took part; accounting for some 46% of estimated global refined tin use in 2016. Key headline findings from this report are as follows:

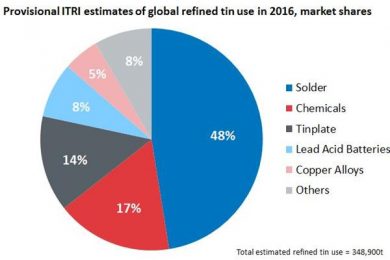

- ITRI’s latest estimate of refined tin use in 2016 is 348,900 t, based on data from the 2017 survey. The figure is just 1,200 t lower than the preliminary 2016 estimate made following last year’s survey. Refined tin demand reported by survey participants increased by 3.3% from 2015 with more modest growth anticipated in 2017

- Solder still accounts for the largest global share of tin use, recovering into growth from a long-term low in 2015. China powder and paste producers were particularly positive. The automotive sector is likely to be a key driver, as well as new markets such as solar solders, although miniaturisation is still a threat and many respondents expected future solder sales to be static or in decline

- Tin use in chemicals grew by 5.5% in 2016 and is expected to increase outside China in 2017. The sector in China was temporarily impacted this year by government environmental inspections. Tin price and competition are still significant issues but threats from regulation may have receded as PVC and other polymer markets have grown strongly. Traditional markets for inorganic products remain static or in decline

- Provisional estimates of total global tin use including refined and unrefined forms totalled 422,900 tonnes in 2016, up 1.7% from 2015. The Recycling Input Rate (RIR) was calculated as 30.7% in 2015, down from 31.4% in 2014

- Pipeline refined tin stocks held by surveyed companies at the end 2016 amounted to the equivalent of 3.39 weeks’ supply. If this ratio is extrapolated based on global consumption it would imply that world consumer stock holdings were around 23,000 t.