At the CRU 15th World Copper Conference earlier this month, during CESCO week in Santiago, Chile, Aston Bay Holdings’ President & CEO Benjamin Cox spoke about the expected changes in the global copper supply and participated in a panel titled Financing Tomorrow.

Commenting on the conference in general Cox said “my view completely disagrees with the consensus view of the industry experts whom I saw presenting at the CRU Conference. After two days of listening to copper experts, I think that they mostly agree with each other. They generally believe that the copper market is going to be in slight surplus for two to three years, with 150,000-300,000 t of extra metal per year. I personally think they are too narrow in their range of possible targeted outcomes.

“For the record, I agree that the copper market is going to be driven by China, but where we disagree is what happened in China last year. I see 2015 as having been a year of serious destocking of industrial inventory. In a business where a commodity price is in free fall, and where the broader stock market was also in free fall, most everyone will move to cash on their balance sheet, rather than metal in a warehouse.

“If I am half right and there was even 500,000 t of industrial global destocking last year, and 2016 demand is either flat or up 1-3% with 2015 (which is the consensus), we are going to face a 350-500,000 t shortfall. If I am completely correct copper could be on an electrifying path to a serious recovery.

“The second place where I disagree with the ‘street’ is that copper demand is going to be correlated with historical steel and cement demand. My view is that as the Chinese shift to more copper intensive luxury goods (better cars, more wired apartments, etc.) they could double their copper demand over the next 10 years while keeping steel demand flat.

“’Industry experts’ are driving long-term investments with their short-term market predictions. In the best case for the copper market, the miners believe the ‘experts’, cut back production as it is not ‘needed’ and the Chinese do what I think they will do, which is restock the industrial supply chain or at a minimum buy the metal they need to keep up with demand.

“If that happens than 2016 is going to be an interesting year.”

His presentation Change in Copper Supply: What do we face in ten years? gives additional reasons for Aston Bay’s bullishness:

- Large, new low-grade porphyries are not going to work in the next 10 years, and outside of that there are very few things to look at

- Supply will be more constrained as companies don’t reinvest into mature operations beyond the minimum needed to maintain current production

- Political risk, water risk and declining grades all require significant investment, but balance sheets of operators are often stretched

- Demand is not price-constrained; when was the last time someone decided not to buy a refrigerator or car because of the price of copper?

- In the long-term, copper will be supply-constrained rather than demand-driven.

He concluded with the five core drivers of supply in the copper industry:

- Scarcity or oversupply of water

- Political and nationalisation risk

- Dwindling mine grade

- Limited feasible discoveries

- Inconsistent capital flow.

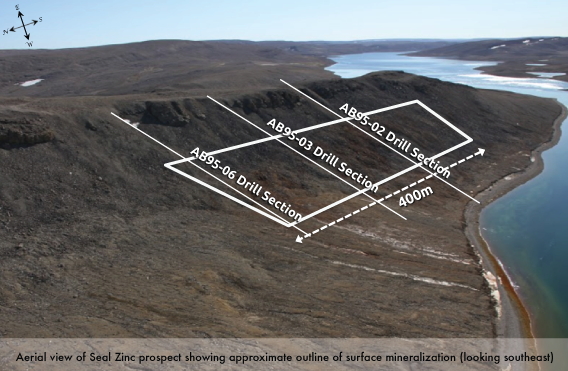

Aston Bay Holdings is focused on the 395,118-ha Aston Bay property located on northwest Somerset Island, Nunavut, Canada. The property hosts the Storm copper and Seal zinc (aerial view shown) prospects, where historic drilling has confirmed the presence of sediment-hosted copper and zinc mineralisation.