PGI Intelligence’s latest Insight report is now available on the lithium mining sector in South America. Highlights from this evaluation of the lithium mining environment in South America include:

- “Growing demand for lithium in the next few years will see increasing investor interest in Chile, Argentina and Bolivia, which boast the world’s largest reserves of the mineral

- Bolivia has the largest single deposit of lithium, but rudimentary infrastructure, a challenging regulatory environment and doubts around the security of investments will continue to pose obstacles to investors

- Chile’s lithium industry is the most mature in the Americas, and its reserves of lithium are of higher quality and more easily exploitable than Bolivia’s, yet the constitutional definition of the mineral as a strategic asset has complicated the investment process and could slow future investment

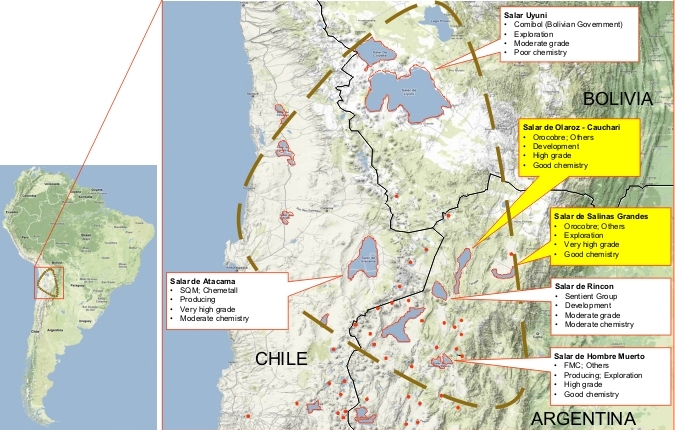

- Regulatory reforms to encourage investment in Argentina’s mining sector will likely speed up lithium industry growth and could see the country have the fastest project growth rates of the ’lithium triangle’ (map courtesy of Orocobre).

“The extent to which the lithium market will grow is contested, but market trends indicate that lithium will be an increasingly profitable sector within mining in the next five years.”

Demand for lithium grew at an average annual rate of 11% between 2010 and 2015, and the price of 99% pure lithium carbonate exports to China – the world’s largest lithium market – more than doubled in the last two months of 2015 alone. This growth in demand is projected to continue due to forecast supply shortages and a predicted increase in demand for lithium-ion batteries for use in electric vehicles and battery-based energy storage.

Joe Lowry, the President of advisory firm Global Lithium, expects global demand for lithium carbonate to rise to between 280,000 and 285,000 t by 2020 from about 163,000 t in 2015, with larger spikes post-2020. Bolivia, Chile and Argentina are likely to become key players in the lithium industry, with the lithium triangle of salars of Uyuni in Bolivia, Atacama in Chile and Hombre Muerto in Argentina accounting for more than 70% of known world reserves. All three countries have made clear they intend to invest in and develop their lithium deposits, offering a mix of different opportunities and obstacles for investors.

Bolivia’s Salar de Uyuni contains the largest known reserve of lithium in the world, but presents a challenging operating environment that will require significant start-up costs. “Located in a remote location some 3,600 m above sea level with little surrounding infrastructure, the transport of product from Uyuni will be costly, not least given that Bolivia lacks a seaport. Moreover, the type of lithium at Uyuni requires a consistent supply of chemicals for the processing of brine, the transport for which will be hindered by the region’s poor accessibility. In order to become a viable production site, the salt flat will require the construction of first rate infrastructure and the bringing in of both technology and skilled labour from outside the area. Although no specific local content requirements on lithium mining have been announced, the government’s strict general local content requirements of a maximum 15% of foreign employees create an additional obstacle.

“High levels of state control over lithium mining and a burdensome tax regime also present hurdles to investment in Bolivia’s lithium sector. The government has pledged $925 million of investment in lithium and has stated that it will only partner with foreign companies willing to provide technology and expertise in the processing phase of lithium on Bolivian soil as part of efforts to develop a domestic added-value industry of higher value goods. Previous proposals to exploit lithium reserves from foreign companies with substantial expertise in lithium battery and electric car technology including France’s Bolloré, South Korea’s LG Group and Japan’s Mitsubishi and Sumitomo have so far failed to materialise. A letter of intent was signed between the Bolivian government and French Atomic Energy and Alternative Energies Commission (CEA) in 2014 to explore cooperation around the lithium industry but few details of these developments have subsequently emerged. President Evo Morales has also stated the government aims to retain at least 60% of revenues from any partnership arrangement.

“Investment security will remain a concern in light of the previous nationalisation of foreign mining companies and the limited investor protections provided by the 2015 law on arbitration. In 2012, the government nationalised Glencore’s Colquiri tin and zinc mine and South American Silver’s Malku Khota silver-indium mine. The nationalisation of Malku Khota was justified on the grounds of violent civil unrest, which could serve as a future pretext for nationalisation as lithium mining could see a resurgence in civil unrest if community engagement efforts fail or environmental impact and intensive use of water are not managed. Government law offers no guarantees of investment security, as the 2015 law on arbitration stipulates that disputes arising from investment in natural resources are not subject to arbitration. In the event of expropriation, the government has generally bided by the rulings of international arbitrations, but these are lengthy and were made considerably more risky for investors by Bolivia’s withdrawal from the International Centre for Settlement of Investment Disputes in 2007.

“Despite the aforementioned political challenges, the long-term outlook for investment in Bolivian lithium could change with the 2019 general election, when President Evo Morales is constitutionally required to leave office. Although levels of political risk to mining in a post-Morales government are unknown at this time and could remain under future Movement for Socialism (MAS) leadership, some companies viewing Bolivia’s lithium mining prospects are likely already considering engagement in the sector, especially in light of the long-term investment cycle for mining projects. The success of the government’s current pilot lithium development program with Germany’s K-Utec and its ability to engage foreign partners in joint development projects will be indicative of wider investor appetite and the prospects for mineral processing in Bolivia more broadly. The growing interest of manufacturing companies dependent on lithium to engage in the production phase and secure longer-term contracts guaranteeing supply at more stable prices could incentivise some to invest in such joint ventures.”

High quality reserves, a favourable investment climate and existing industry and transport infrastructure will aid the development of Chile’s lithium sector in Salar de Atacama. Investors could also benefit from Chile’s expertise in the mining process, which first began to produce lithium carbonate in 1984.The country was the second largest lithium producer in the world in 2015, behind Australia.

“Despite the benefits offered by Atacama, regulations around lithium investment present a potential disincentive for investors. The government considers lithium a strategic material, making the award of concessions a more heavily regulated and politically divisive process. The government’s first ever tender for a special lithium contract in 2012 was a failure, with a concession awarded to domestic chemical company SQM cancelled shortly afterwards due to irregularities in the bidding process. An ongoing contractual dispute between SQM and the Chilean government also highlights the potential legal difficulties that concession holders may face. SQM is currently engaged in arbitration with the government Economic Development Agency, Corfo, after it threatened to revoke SQM’s licence, accusing the company of underpaying royalties and market manipulation. SQM meanwhile insists it has always complied with contractual obligations.

“Government exploration of public private initiatives to develop the lithium industry could facilitate a more open investment climate for private companies in Chile’s lithium sector. Santiago will be keen not to lose out market share to other emerging lithium producers such as Argentina and in February 2016 agreed with Albemarle Corp – which acquired Rockwood in 2015 – to almost triple production at facilities in Salar de Atacama and Sector La Negra. The move is opposed by SQM, which asked local authorities to invalidate the deal alleging serious violations of environmental regulations during the evaluation process in May 2016.The public reaction to increased private investment in lithium could also influence the pace of reform in the sector while the activities of state mining company Coldelco, which holds two existing concessions, will be illustrative of the level the government intends to participate in lithium in upcoming years.”

By contrast, political change with the election of President Mauricio Macri in December 2015 and the improving legislative landscape for mining companies could see rapid growth in Argentina’s lithium industry. Known lithium reserves are concentrated in the provinces of Salta, Jujuy and Catamarca, and benefit from similar geological conditions to the lithium-rich salt flats in Chile, with higher quality lithium and rapid brine evaporation rates.

“Since assuming office in January 2016, President Macri has undertaken a series of reforms to improve the investment climate, including the elimination of currency controls which previously complicated the repatriation of profits, and the removal of a 5% tax on mining exports.

Argentina’s Mining Code gives each province autonomy in determining the strategic status of lithium, which in turn determines if concessions can be granted to private investors. Companies with total or near-total ownership of lithium concessions include Dajin Resources (see next issue of International Mining Project News), which holds a 100% stake in the Salinas Grandes lithium site in Jujuy, and Galaxy Resources, which has a 96% stake in Sal de Vida.

“FMC Corp, which already operates in Argentina, has expressed optimism around the investment climate in Argentina’s lithium sector under the Macri administration, in line with wider investor sentiment regarding Argentina’s natural resources. The speed of development of projects such as the Olaroz facility operated by Orocobre and the Western Lithium project – due to begin production next year – will provide early indicators of the market’s growth.

Protection Group International (PGI) is a London-based risk management consultancy specialising in geopolitical intelligence and corporate investigations, cyber security, and capacity training.