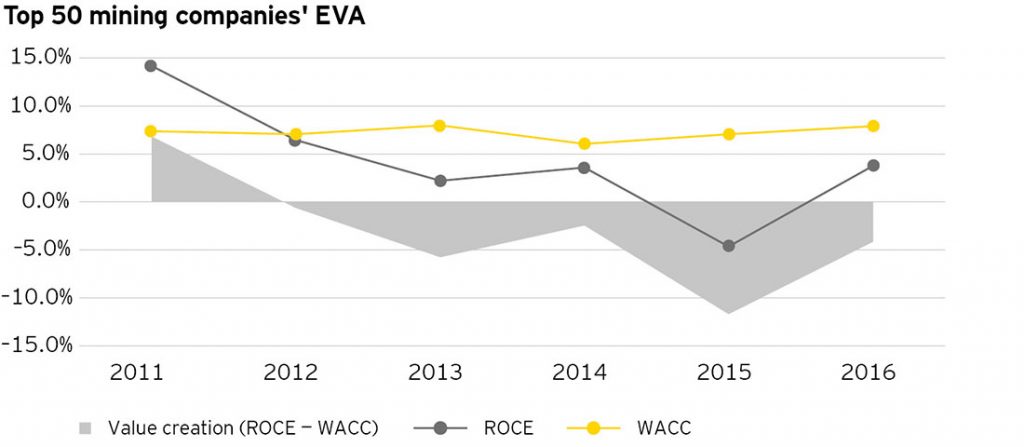

Mining companies’ economic value creation is set to rebound in 2017 after consistent erosion since 2011, according to the second report of a new EY two-part series, Does cutting debt have to mean reducing your ambitions? Debt reduction and relentless cost-cutting remains high on the agenda, however, as the mining and metals sector seeks to create shareholder value through margin improvement and lowering financial risk in the wake of 2016’s uptick in commodity prices.

The report analyses the world’s top 50 mining companies by market capitalisation and reveals that debt fell by around 15% year-on-year in the first half of 2017. If this trajectory continues, debt/EBITDA could be set to fall below 1.0 for the first time in five years according to the report. The survey findings also highlight a continued shift in capital structure for the mining and metals sector, with gearing dropping to 32% at the end of the first half of 2017 – two percentage points lower than that at the start of the year.

Lee Downham, EY Global Mining & Metals Transactions Leader, says: “The trend toward continued debt reduction and shareholder returns reflects a persistently cautious mindset across the mining and metals sector. But the return to growth is now offering flexibility to apply other levers to create value, such as production growth, restructuring of portfolios and better cash allocation to improve valuation multiples. A balanced approach to capital allocation, which not only considers the need to return cash to shareholders but also the need to grow, is necessary to enhance shareholder value creation. Many players will now be assessing the efficiency of their capital structure given its implications on the overall cost of capital and shareholder value creation.”

Continuing change in capital structure is supported by the latest EY Mergers, acquisitions and capital raising in mining and metals: 3Q17 trends and 2017 outlook, which indicates that appetite to raise more capital in the sector is expected to increase as the switch to growth gains momentum. According to the report, global aggregate capital raised increased by 8% year-on-year to $66 billion in 3Q17, with China’s share increasing to 41% of the capital raised from 25% in the previous quarter. There also was an increase in activity in equity markets in 3Q17, with follow-on equity more than doubling quarter-on-quarter to US$12.5b, up 66% year-on-year.

M&A activity showed similar signs of improvement, marked by some evidence of a shift from largely divestment-led drivers to strategic-led deals focused on growth. Despite a fall in deal value of 42% in 3Q17 quarter-on-quarter to US$9.4b, deal value over the first nine months increased by 68% year-on-year. Chinese activity increased to 37% of deal value in 3Q17, up from 20% in 2Q17, and deals targeting established mining regions in Australia and North America comprised 60% of the volume of deals undertaken in 3Q17.

Downham concludes: “Deal activity appears to be increasing, as investor concerns shift away from financial risk and begin to focus on how companies create long-term value creation. We anticipate that consolidation deals will be fueled by the availability of capital and a growing threat of intervention from activist investors. The focus on lowering financial risk should also ease going forward, with activity in debt markets picking up once again.”