Orca Gold Inc and Resolute Mining Ltd have closed the second of two tranches of a previously announced private placement. “In six years, commented Rick Clark, CEO and Director of Orca Gold, “we managed to discover the Block 14 gold project, significantly de-risk it and demonstrate Sudan’s merits as a favourable mining jurisdiction with a vast gold endowment. We are excited as we enter the final leg of completing the feasibility study on what looks to be one of the largest undeveloped gold projects in Africa. On behalf of Orca’s board of directors and management team, I thank Resolute again for its vote of confidence and recognition of the work we have done. In addition to the delivery of the feasibility study, Orca will continue to uncover the potential of our property in Sudan and concessions in Côte d’Ivoire with ongoing exploration efforts in both countries. We look forward to delivering the results from our programs to the market in due course.”

As a result of the closing of the Second Tranche, Resolute has increased its ownership from approximately 9% to some 17% of the current and undiluted issued and outstanding shares of Orca.

Resolute’s Managing Director, John Welborn, was pleased to support Orca’s exploration and development ambitions: “Orca is among the first movers in a region which is host to a modern-day gold rush. We have been impressed with the work completed to date at the Block 14 gold project by the company’s well credentialed management team and we look forward to unlocking further value.”

Net proceeds of the Private Placement will be used to provide Orca with additional funding for optimization of the ongoing feasibility study on Block 14. Continued success of resource expansion based on a new geological interpretation (see Orca news release on May 1, 2018) has resulted in a decision by Orca’s Board of Directors to extend the delivery of the feasibility study to Q4 2018.

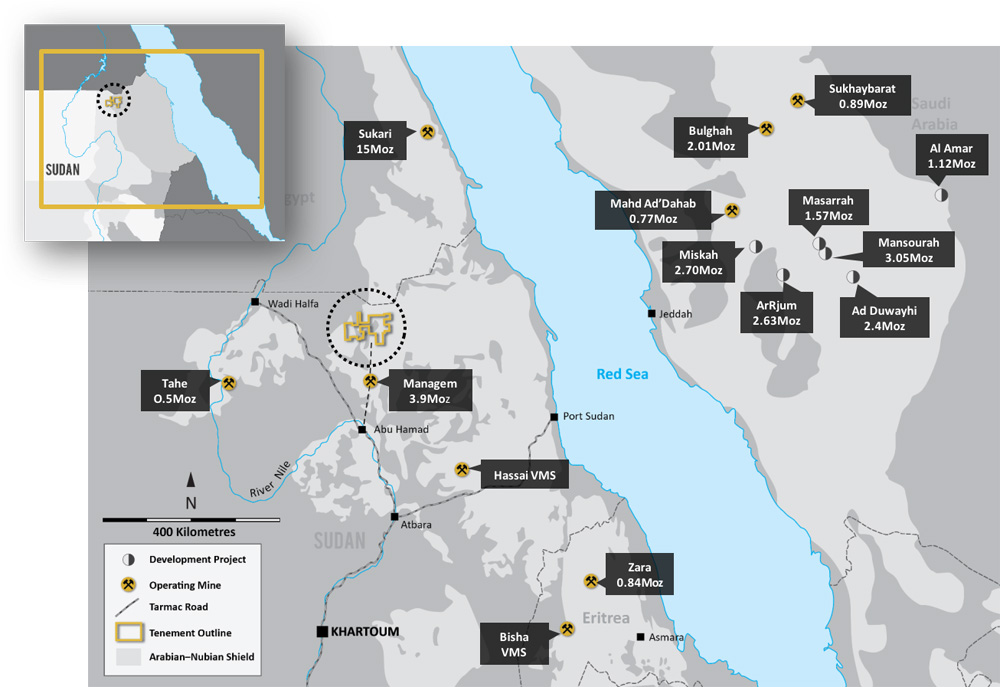

The Block 14 gold project is located close to Sudan’s border with Egypt, 900 km north of the capital Khartoum. The Block 14 concession covers 2,170 km2. Access to the project is by sealed road along the eastern bank of the River Nile to the town of Abu Hamad and then via a well used desert road to the project area.

Using a gold price of $1,100/oz for mine design, and $1,200/oz for economic analysis, highlights of the revised PEA announced in May 2017 include:

| Pre-tax NPV7% | US$ 278.2 M (+78% from Jul ’16 PEA) |

| Pre-tax IRR | 26.5% |

| After-tax NPV7% | US$ 227.7 M |

| After-tax IRR | 23.1% |

| In-Pit Mineral Resources* | INDICATED: 41.0Mt grading 1.46g/t for 1,928 Koz (+57% from Jul ’16 PEA) |

| INFERRED: 3.4Mt grading 1.56g/t for 173 Koz (+25% from Jul ’16 PEA) | |

| Life of Mine (LOM) | 13.2 years |

| Avg. LOM Production | 135,000 oz Au/year |

| Avg. Gold Recovery | 84.5% |

| Cash Cost | US$701/oz for LOM |

| All-in Sustaining Costs | US$ 752/oz for LOM |

| Initial CapEx | US$211 M (including 25% contingency) |

| Sustaining CapEx | US$ 92 M |

| Payback Period | 3.0 |