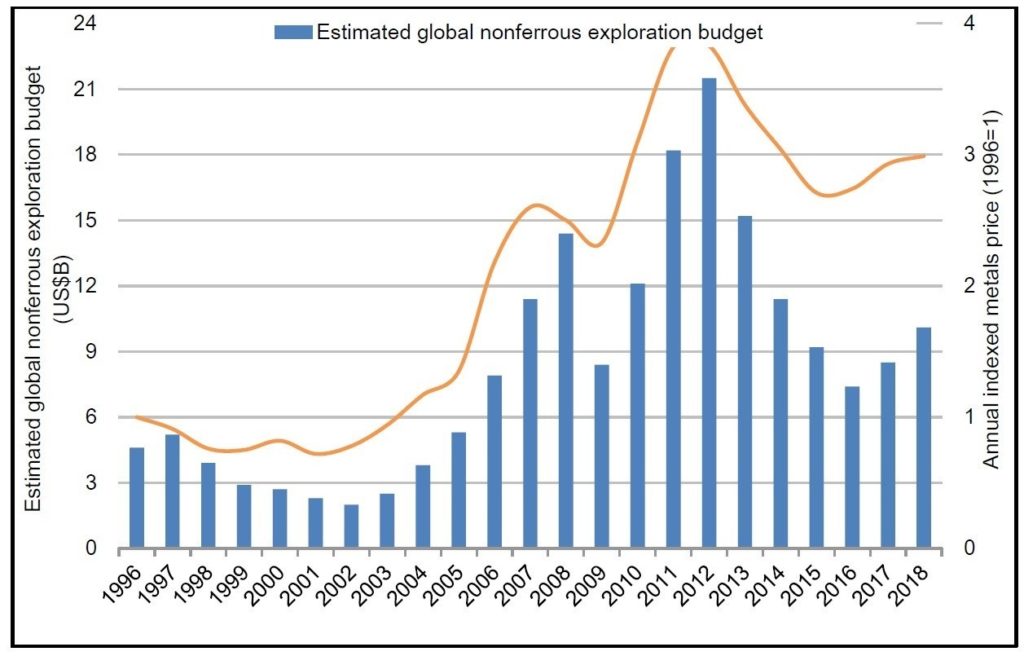

S&P Global Market Intelligence report highlights global nonferrous exploration budgets increased for the second consecutive year, up 19% year-over-year. Key takeaways:

•Global nonferrous exploration budget increased 19% to $10.1 billion

•Junior exploration companies budgets increased by 35%

•Number of active exploration companies increased for first time since 2012 — up 8% to 1,651

•Cobalt & lithium budgets continue to rise, up 500% since 2015

•Canada, Australia and the U.S. all record above-average increases.

Mark Ferguson, Associate Director of Metals & Mining Research at S&P Global Market Intelligence, says: “Improved metals prices and margins since 2016 have encouraged producers to expand their organic efforts the past two years. Over the same period, equity market support for the junior explorers has improved, leading to an uptick in the number and size of completed financings. This allowed the group to increase exploration budgets by 35% in 2018.

“Our data does show that, despite these improvements, the level of equity market support and industry-wide exploration efforts remain far below peak levels recorded from 2010 to 2012.”

The improved investment environment has, for the first time since 2012, finally resulted in more dormant companies resuming exploration efforts and new entrants into the industry. The 1,651 companies actively exploring in 2018 is 8% more than the 1,535 companies with budgets in 2017. However, the 2018 total is still about 900 companies less than in 2012, representing a one-third culling of active explorers over the past five years.

Global attention on raw material needs for the Electric Vehicle revolution has attracted significant interest from the exploration sector. Exploration budgets for cobalt and lithium, key commodities for a variety of batteries, have collectively risen by more than 500% since 2015, including an 82% increase this year. However, these allocations remain relatively small when compared with planned exploration allocations for traditional base- and precious metals-focused efforts.

Although gold prices have been fairly unremarkable since 2017, generally trading within a $100/oz band, gold continues to benefit the most from the industry recovery. Gold explorers have increased their aggregate budget to $4.86 billion in 2018, up from $4.05 billion in 2017. Although lagging behind the gold allocation total, base metals allocations have also made a significant move upwards this year, increasing by more than $600 million to $3.04 billion. Copper remains by far the most attractive of the base metals, although zinc allocations have increased the most, rising 37% in 2018. Budgets are up for all targets except uranium.

With a budget of $1.44 billion, Canada remains the top destination for nonferrous exploration budgets in 2018; the 31% year-over-year increase in allocations for the country outpaces the 23% rise in budgets for second-place Australia, which has attracted $1.33 billion. In third-place, the US has recorded a 34% increase in allocations. In each of these countries, gold’s share of the total is more than 55%.

Of the remaining 10 most popular exploration locations, four are found in Latin America, including Peru, Mexico and Chile, which hold the fourth through sixth positions globally.