US coal exports totalled 8.18 Mt in February, up 2.9% from January and up 30.6% from the year-ago month, US Census Bureau data shows. The slight gain in monthly volumes from January occurred despite a drop in thermal coal volumes, which totaled 3.3 Mt in February, down 12.1% from January but up 17.8% from the year-ago month.

Thermal coal export volumes dropped as the price for S&P Global Platts CIF ARA assessment for delivered thermal coal into Northern Europe (basis 6,000 kcal/kg NAR, loading 15-60 days), averaged $83.96/t, down from $95.02/t in the prior month.

Top destinations for thermal coal in February were India at 573,033 t, up from 236,126 t in the year-ago month; South Korea at 453,489 t, up from 307,981 t in the year-ago month; and Egypt, which took delivery of 331,872 t in February, up from zero tons in February 2017.

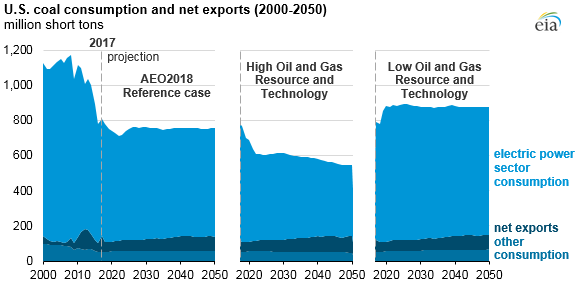

Meanwhile, the EIA projects US coal disposition – domestic demand and coal exports – to remain relatively flat through 2050 in the Annual Energy Outlook 2018 (AEO2018) Reference case, even as many coal-fired power plants are retired. Coal disposition for the next three decades averages 750 Mst/y, down from the peak of nearly 1.2 billion st in 2008.

Coal demand in the power sector is sensitive to changes in the price of natural gas, and two sensitivity cases with higher or lower natural gas prices show the effects of this relationship. The AEO2018 Reference case is based on current laws and regulations. Changes in policy could significantly affect coal use.

Overall, coal disposition is mostly affected by changes in the electric power sector, where 82% of domestic coal was consumed in 2017. US power sector consumption of coal depends on the amount of coal-fired generating capacity and the utilization rate of that coal generation fleet. Coal’s competition with other electricity-generating fuels, in particular natural gas, has implications for both capacity retirement and utilization decisions.